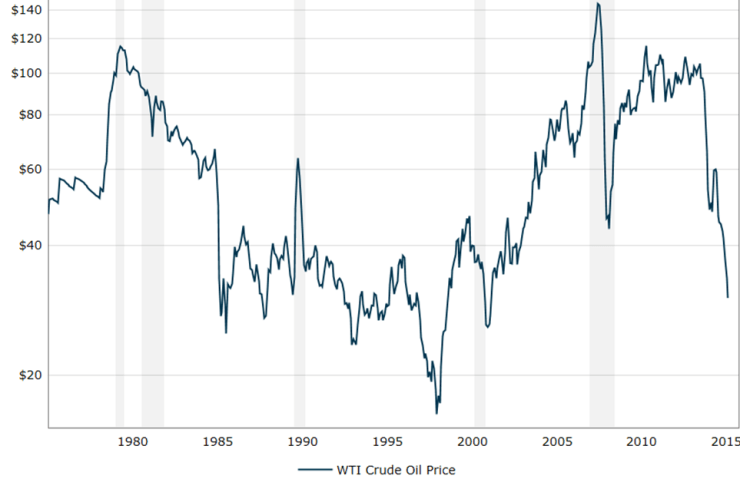

Oil and Gas industry in Norway has faced great challenges due to “unforeseen” decrease in oil price. High production cost combined with high labor cost has resulted in companies freezing new projects and pushing investments as far into the future as possible.

The reason I used term “unforeseen” in quotation marks is because it really was unexpectedly strong and sudden decrease but after all it was nothing new for the extremely volatile material.

Fig 1. Inflation corrected WTI Crude Oil Price 1976-2015 on logarithmic scale.

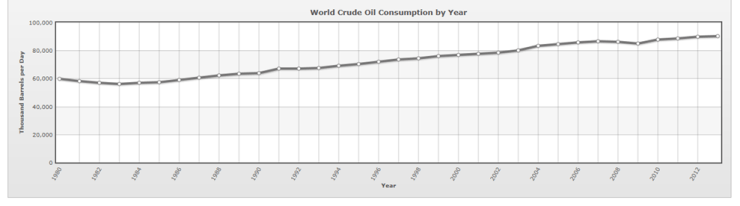

New oil reserve discoveries, new extraction methods, wars and global growth and decline have altered the barrel price throughout the history. However, one thing has been relatively stable: the growth of global oil consumption. Regardless of the oil barrel price or macro economical situation the oil consumption has been steadily increasing over the past decades.

Fig 2. World Crude Oil Consumption 1980-2013.

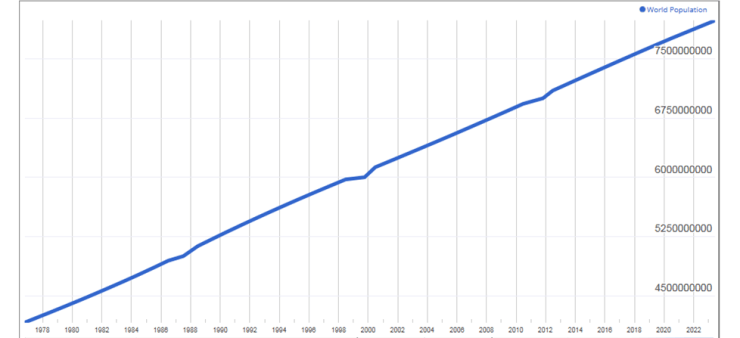

The simple reason for the growth in consumption is the growth of global population. Despite we are finding new sources of energy and we are making products and services more efficient, the growth rate of our population is increasing the demand for oil.

Fig 3. World population, past, current and estimation.

One does not need a degree on forecasting to foresee that there is growing number of people in Asia, Middle East and especially in Africa waiting to hike their living standards towards what we are used to in the western countries. This will ensure the demand growth for oil for decades to come despite good development on new sources of energy and even more efficient usage of oil.

So how does this relate to the title of this blog post?

We have seen, and it is justified to forecast for the future as well, that growth in global population is increasing the oil demand. We have also seen that increase in oil demand has not steadily increased the oil price but more of its volatility.

For the Norwegian Oil and Gas industry this results as need for flexible operations. As investments within the Oil and Gas industry have expected life time in decades rather than years the market turbulence is not a show stopper. However, the market turbulence is defining the quarterly and yearly results and here is where We at Ramirent can assist You. We can increase Your flexibility on operations and turn Your CAPEX investments into manageable and flexible OPEX. Our high quality and robust products combined with services are available when You need it and where You need it.

Let us help you to manage the volatility and fight the market turbulence.

Sincerely,

Jarkko Tiainen

KAM, Oil & Gas, Ramirent Norway

Jarkko.antero.tiainen@ramirent.no

+4791842161

Officially published at Ramirent Oil&Gas Blog

Ramirent offices in Western Norway:

Hordaland

| Ramirent Bergen – Blomsterdalen | (+47) 55 70 70 70 |

| Ramirent Bergen – Minde | (+47) 55 70 70 71 |

| Ramirent CCB Ågotnes | (+47) 55 70 70 73 |

| Ramirent Stillas – Bergen | (+47) 55 70 70 74 |

| Ramirent Stord | (+47) 53 40 31 00 |

Rogaland

| Ramirent Haugesund | (+47) 52 80 60 30 |

| Ramirent Module Systems AS | (+47) 51 71 56 20 |

| Ramirent Stavanger | (+47) 51 95 87 00 |

| Ramirent Stavanger Stillas | (+47) 40 01 75 67 |

Sogn og Fjordane

| Ramirent Førde | (+47) 57 82 70 00 |

| Ramirent Sandane | (+47) 57 86 88 50 |

| Ramirent Sogndal | (+47) 57 67 56 50 |

References:

Fig. 1: http://www.macrotrends.net/1369/crude-oil-price-history-chart

Leave a comment